Industrial Sector Is The Leading Commercial Real Estate Asset Category

During this era of social distancing and confinement, anyone who has been purchasing groceries online has experienced the challenges with delivery […]

During this era of social distancing and confinement, anyone who has been purchasing groceries online has experienced the challenges with delivery […]

March 30, 2020 A frequent question consistently raised during these tumultuous times is how to handle a tenant seeking to renegotiate its rent payments

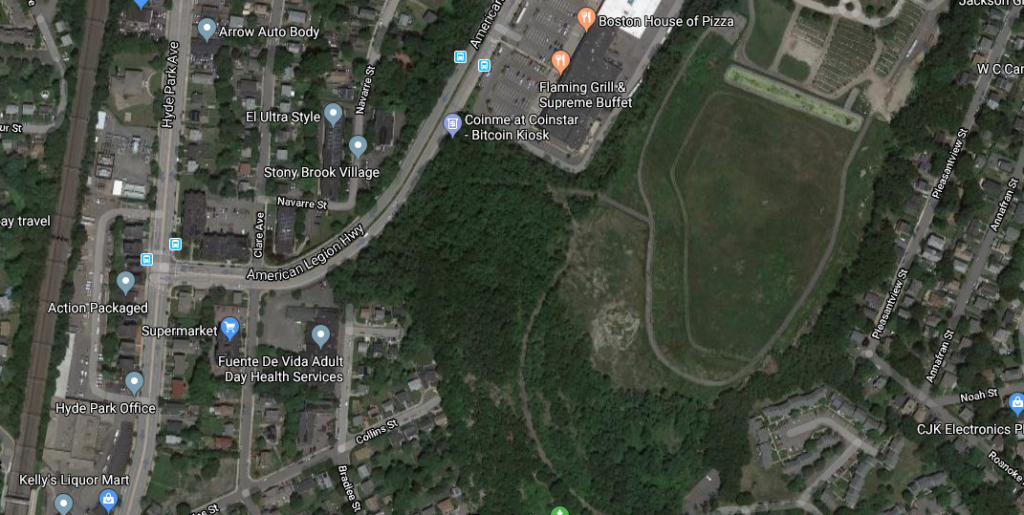

23.34 acre development site within the City of Boston located at American Legion Highway, Cummins Highway and Hyde Park