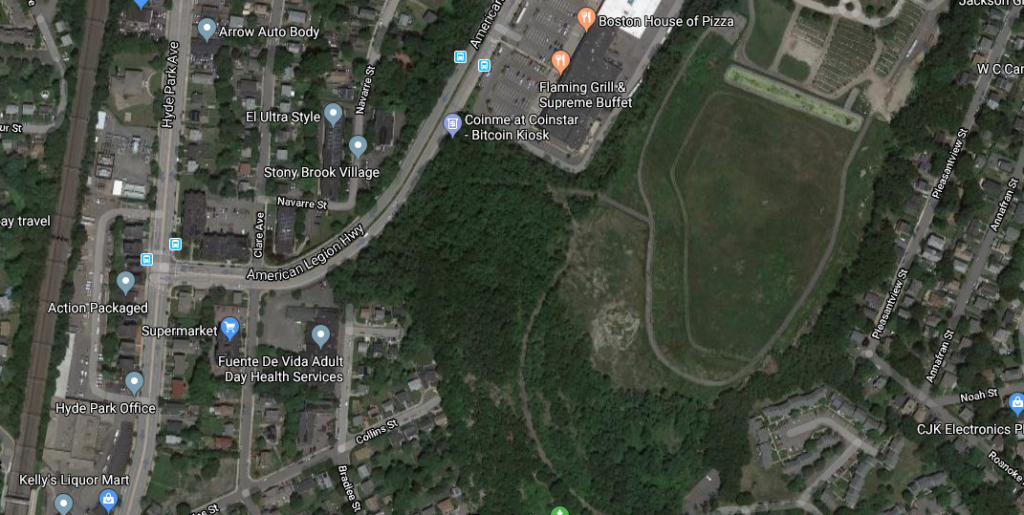

Victoria Heights, Roslindale

23.34 acre development site within the City of Boston located at American Legion Highway, Cummins Highway and Hyde Park […]

23.34 acre development site within the City of Boston located at American Legion Highway, Cummins Highway and Hyde Park […]

1/8/19 The risks to the downside for the commercial real estate market are currently outweighing the upside as negative indicators

Actually, WeWork wants to do more than just conquer the real estate market. The ambitious plans for this rapidly growing

Equity markets typically disdain uncertainty yet, as of this writing, the S&P is up about 6% since the US

The most effective commercial real estate brokerage firm provides a full spectrum of services to its clients. Companies that require

A role I have found that I thoroughly enjoy is assisting business owners with finding solutions to their real estate requirements.

The current economic climate has enabled strong demand for business owners to seek commercial properties to acquire to accommodate their real

As described in Part I: “What does Triple Net and Gross Mean?,” a triple net lease means that the tenant